You've built the business one job at a time. First it was you, a van, a phone, and a long list of problems to solve. Then came apprentices, office staff, more vehicles, better systems, and the point where the business started to feel like something bigger than your own daily labour.

Now you're thinking about selling.

For most plumbing owners, that thought doesn't arrive in a boardroom. It shows up on a late drive home, after another emergency call, or when you realise you've built something valuable but haven't worked out how to turn it into a clean exit. You want a fair price. You want your team looked after. You want the handover to work. And you don't want to spend months talking to the wrong buyers while the business suffers.

Selling well is rarely about finding one enthusiastic buyer and naming a number. It's about preparing a business that a buyer can understand, trust, and run after you step back. That's the difference between a deal that closes and one that falls apart in diligence.

Table of Contents

- Thinking About Your Next Chapter

- Getting Your Business Ready for a Buyer

- How to Value Your Plumbing Business Accurately

- Packaging Your Business to Attract Buyers

- Choosing Your Path to a Sale

- Vetting Buyers and Navigating Negotiations

- Closing the Deal and Planning Your Exit

Thinking About Your Next Chapter

A lot of owners start with the wrong question. They ask, “What's my plumbing business worth?” before they ask, “What exactly am I selling?”

If the business still depends on you to quote jobs, calm down difficult customers, handle emergency calls, approve every purchase, and keep the team moving, a buyer won't see a business first. They'll see a job with overhead attached. That's the hard truth.

The owners who sell well usually reach a point where they want one of three things. They want to retire. They want to step out of day-to-day operations. Or they want to take chips off the table after years of carrying risk. Those motives are all valid, but they lead to different sale decisions.

The personal side matters

Selling a plumbing business isn't just a financial event. It's also a transfer of responsibility.

You're deciding what happens to your staff, your customers, your name in the local market, and the systems you've spent years building. If you don't get clear on your own priorities early, you can end up chasing the highest number and regretting the buyer behind it.

A simple starting point is to write down your essential conditions:

- Your timeline: Do you want out quickly, or can you prepare properly?

- Your role after sale: Are you happy to stay on for a handover, or do you want a short transition?

- Your team: Which people do you want protected or retained?

- Your deal priorities: Is your focus price, certainty, legacy, or a mix of all three?

A good sale isn't only the highest offer. It's the offer that still makes sense after diligence, legal review, and handover.

What usually goes wrong at this stage

Owners often delay too long, tell too many people too early, or assume a strong revenue number is enough. It isn't. Buyers care about profit, transferability, and risk.

If you want to learn how to sell a plumbing business properly, start by treating the exit like a project. That means planning it, staging it, and taking emotion out of the process where you can. You'll still care immensely. You just can't let that care turn into guesswork.

Getting Your Business Ready for a Buyer

A plumber decides to sell after a tough winter, a sore back, or a better offer than expected. Then the buyer starts asking for job costing, service agreement retention, staff roles, and proof the business can run without the owner answering every second phone call. That is the point where preparation stops being theory.

A sale process usually works better when the business is cleaned up well before it goes to market. Buyers pay for what they can verify. In a plumbing business, that means repeatable profit, dependable service revenue, and an operation that does not fall apart when the founder steps out.

Start with the buyer's risk checklist

Buyers in the trades tend to look past the sales pitch quickly. They want answers to a short list of practical questions.

Can the office run without you for a week?

Can another person quote work using the same pricing logic?

Do service customers belong to the company, or to you personally?

Will technicians stay after handover?

Are the numbers clean enough to survive due diligence?

Those questions get to the heart of transferability. A plumbing business with strong revenue can still be hard to sell if the owner is the dispatcher, lead estimator, rainmaker, and relationship manager all at once.

What to fix first

I tell plumbing owners to sort the business in the same order a buyer will test it.

- Clean up the financials: Separate personal spending from business spending. Make owner add-backs easy to identify and support with records.

- Document how work gets done: Put quoting, dispatch, invoicing, warranties, call handling, after-hours response, and collections into written procedures.

- Define who owns each function: Buyers want to see clear responsibility across the office, field supervision, estimating, and customer communication.

- Organise compliance records: Keep licences, insurance, permits, vehicle files, maintenance logs, and supplier agreements current and easy to produce.

- Show your service revenue clearly: If you have memberships, maintenance plans, or repeat service agreements, track renewal rates, average ticket, and churn in a way a buyer can follow.

That last point matters more in plumbing than many owners realise. Recurring service revenue often supports a stronger valuation, but only if you can prove those customers are likely to stay after the sale.

For owners tightening their systems before a sale, using apps for plumbing business owners can help standardise communication, scheduling, and reporting across the team.

Reduce owner dependency before buyers see the business

At this point, deals either hold up or start losing value.

If key builders only trust your mobile number, if larger quotes live in your head, or if the office cannot answer basic job-status questions without you, a buyer sees earnings risk. They will lower the price, ask for an earn-out, or walk away.

The fix is operational, not cosmetic.

What that looks like on the ground

- Shift relationships into the team: Bring supervisors, office staff, or senior techs into important customer accounts before a sale process starts.

- Standardise pricing: Build quote templates, margin rules, approval thresholds, and documented exceptions.

- Move knowledge into shared systems: Supplier contacts, preferred parts, warranty workflows, and repeat-job notes should not sit in one person's memory.

- Put visible leaders in place: Buyers gain confidence when they can identify the people who will steady the business after handover.

A simple test helps. Step away for two weeks. If jobs stall, quotes back up, or customer issues pile up until you return, the business needs more work before it is ready for market.

Clean records beat a polished pitch

Many owners spend too much time on branding and too little on evidence. Buyers do not pay more because the brochure looks sharp. They pay more when the records support the story.

In practice, that means clear financial statements, tidy payroll records, documented processes, defensible service agreement data, and a straightforward explanation of how the business wins work and keeps customers. A plain presentation with clean records will usually beat a slick presentation with gaps all through it.

The goal is simple. Make it easy for a buyer to see how the plumbing business makes money, who keeps it running, and why it should keep performing after you leave.

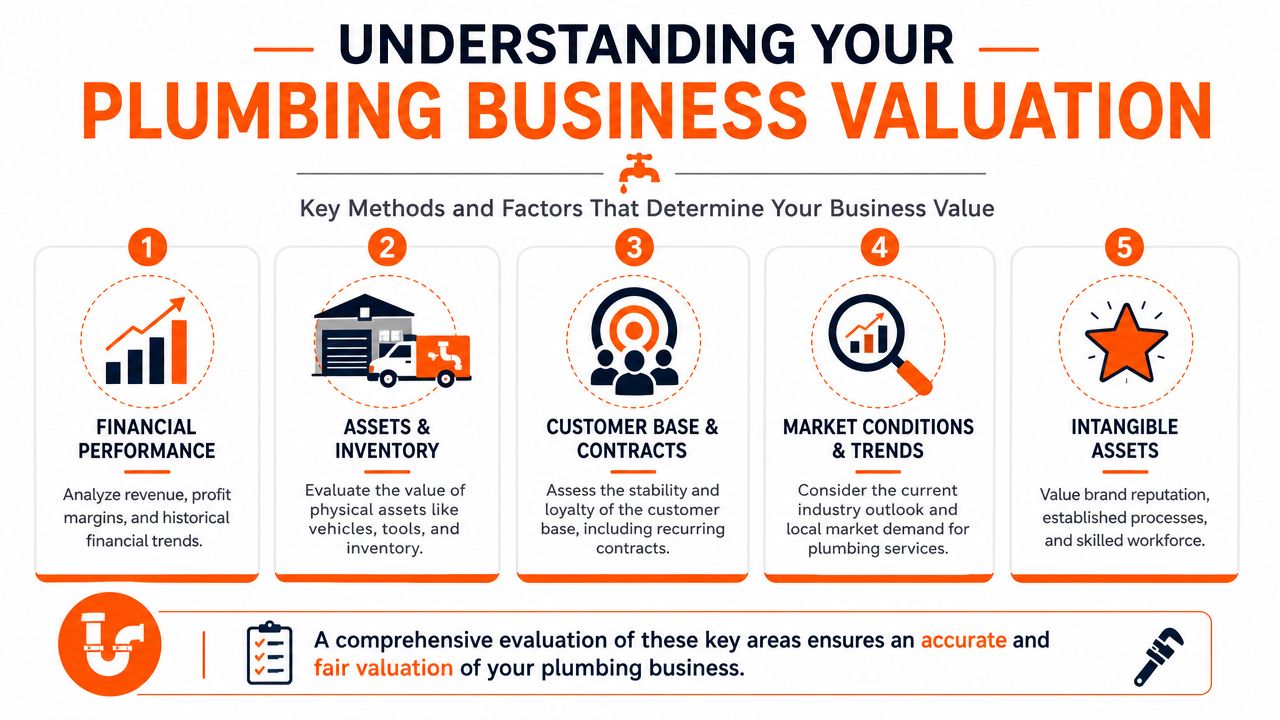

How to Value Your Plumbing Business Accurately

A plumber gets an offer over lunch, then spends the drive back to the shop wondering if it is strong or light. That usually happens because the owner knows the workload, the reputation, and the sacrifice behind the business, but has never had to translate that into a sale price a buyer will defend.

Valuation is that translation.

A buyer is not paying for years of hard work. A buyer is paying for future cash flow, adjusted for risk, and for how confident they are that the business will keep producing after the founder steps out. In plumbing, that question gets very specific. How much revenue is tied to service agreements? How much work repeats without the owner answering the phone? Which relationships belong to the company, and which still belong to one person?

What adjusted EBITDA means in plain English

Most plumbing business sales are priced off adjusted EBITDA. That starts with operating profit, then cleans up the number so a buyer can see what the business would likely earn under normal ownership.

In practice, the adjustments usually include owner perks run through the business, personal vehicle costs, above-market or below-market owner pay, one-off legal or repair bills, and unusual expenses that will not continue after a sale. Buyers will test every adjustment. If an add-back cannot be explained clearly and backed up with records, many buyers will ignore it.

That is where owners get tripped up. They hear “add-backs” and assume every discretionary expense increases value. It does not. A buyer will usually accept adjustments that are legitimate, documented, and demonstrably nonrecurring. They will push back hard on anything that looks like ordinary operating cost dressed up as an adjustment.

A simple example

Here is the basic math:

| Item | Example |

|---|---|

| Revenue | $5 million |

| EBITDA margin | 15% |

| EBITDA | $750,000 |

| Value at 3x EBITDA | $2.25 million |

| Value at 6x EBITDA | $4.5 million |

The spread matters. Two businesses with the same EBITDA can land at very different values because the multiple reflects risk, not just profit.

Owners who want to sanity-check the numbers before speaking with buyers can start with a focused plumbing business valuation tool. It will not replace a sale process, but it helps frame the right questions early.

What actually moves the multiple

Higher multiples usually show up when earnings are clean, the office runs in a disciplined way, and revenue is likely to hold after the handover. For a plumbing company, a few factors carry more weight than owners expect.

- Service agreement quality: Buyers look past the top-line count. They want to know renewal rates, average revenue per agreement, cancellation patterns, and whether those customers produce profitable downstream work.

- Revenue mix: A business with a healthy base of repeat service work often looks safer than one that depends heavily on irregular project revenue.

- Owner dependency: If the owner sells every big job, handles escalations, approves pricing exceptions, and keeps key accounts loyal through personal relationships, the multiple usually comes down.

- Gross margin control: Strong sales do not mean much if quoting is inconsistent or job costing is weak.

- Customer concentration: Heavy reliance on a handful of builders, property managers, or commercial accounts raises risk.

- Team depth: Buyers pay more when dispatch, operations, and field supervision are not all flowing through one person.

Service agreements deserve special attention. I have seen owners count every contract as recurring revenue and expect a premium multiple, only to find that the agreements were underpriced, loosely renewed, or barely used to generate follow-on work. Buyers care about the economic value of that base, not the headline number.

What lowers value fast

A few problems drag value down faster than owners expect.

Messy financials are one. Another is weak separation between personal and business spending. Deferred maintenance on vehicles and equipment can also hurt, because the buyer sees future capital spending coming straight at them. The same goes for unresolved licensing issues, thin middle management, and poor visibility into technician performance.

There is also a difference between a profitable business and a transferable one. A plumbing company can post solid earnings and still trade lower if too much of the operation sits in the owner's head.

Price the business for scrutiny

A realistic valuation helps in three ways. It draws in serious buyers, holds up better in due diligence, and gives you a firmer base for negotiation.

Inflated pricing causes real damage. Good buyers walk early, weaker buyers stay around longer than they should, and the process loses momentum once the market senses the gap between the asking price and the evidence. A fair number, supported by clean adjustments and a clear explanation of risk, usually puts more money in the owner's pocket than an ambitious number that cannot survive review.

Packaging Your Business to Attract Buyers

A strong business can still struggle in the market if it's presented badly. Buyers don't just buy numbers. They buy a story they can understand, verify, and imagine operating themselves.

That's why packaging matters.

Build a proper buyer file

The central document is usually the Confidential Information Memorandum, often called the CIM or “the book.” It should explain the business clearly without burying the reader in fluff.

A useful CIM usually covers:

- The business overview: Services, service area, customer profile, team structure, and operating model.

- Financial summary: Clear summaries tied back to real records.

- Why customers stay: Repeat work, reputation, call flow, and service patterns.

- Operational strength: Fleet, systems, key staff, licences, supplier relationships, and workflow.

- Growth angles: Obvious opportunities a buyer could pursue after acquisition.

The best version isn't hyped up. It's credible. A serious buyer should finish reading it and think, “I understand how this company works, why it makes money, and what could improve under new ownership.”

Set up your data room before buyers ask

The CIM gets attention. The data room keeps momentum.

This is a secure folder structure with the documents a buyer, accountant, and lawyer will eventually request. If you only start assembling it after interest arrives, the process slows down and confidence drops.

What to include

- Financial records: Profit and loss statements, balance sheets, tax returns, and any management reports you rely on.

- Asset details: Vehicles, tools, equipment, lease information, and major replacement history.

- People documents: Employment agreements, role summaries, and key manager responsibilities.

- Customer and supplier records: Significant agreements, service contract templates, and major vendor arrangements.

- Compliance material: Licences, insurance, permits, and any records tied to operational compliance.

Tell the truth, but tell it well

There's a difference between spinning a business and presenting it professionally.

If your commercial division is lumpy but your residential service side is dependable, say that clearly. If you've built a solid office function but still hold too much sales knowledge yourself, acknowledge it and show what has been done to reduce that dependency.

Buyers don't expect perfection. They do expect honesty. When sellers hide weak spots, buyers assume there are more waiting behind them.

Choosing Your Path to a Sale

A plumber with 12 trucks, a loyal maintenance base, and solid profit can still choose the wrong sale process and leave money on the table. I see it happen when owners pick the path that feels familiar instead of the one that fits their size, buyer pool, and level of owner dependency.

If you want to see how plumbing companies are positioned in the market, review a few plumbing business for sale listings and buyer-facing examples. Pay attention to what gets highlighted. Recurring service work, dispatcher depth, licensed staff, and how much still sits with the owner all affect which sale route makes sense.

Path one with a business broker

For many plumbing businesses, this is the right middle ground.

A good broker handles outreach, confidentiality, buyer conversations, and the back-and-forth that eats an owner's week. That matters in plumbing because the business still has to answer phones, book calls, manage techs, and keep revenue steady while the sale process runs in the background.

Broker-led sales usually suit owner-operated and small to mid-sized companies. They work best when the likely buyer is another operator, an individual buyer, or a small local group looking for a platform. If the business has strong service agreement income but still relies heavily on the founder for estimating, sales, or staff retention, a broker can still run the process well. The buyer pool is just different, and the story has to be handled carefully.

The trade-off is broker quality. Some are strong on marketing but weak in negotiation. Some know restaurants and retail but do not understand flat-rate pricing, drain work, commercial service, or what buyers care about in a trade business.

Best fit: Owners who want broad buyer reach and practical help managing the sale without turning it into a second full-time job.

Path two with a direct sale

A direct sale can work well when the buyer is already in the picture. Common examples are a son or daughter taking over, a long-term employee buying in, a nearby competitor, or a larger plumbing company that has approached you.

The appeal is obvious. Fewer people involved, less exposure, and in some cases lower fees.

But direct deals have a weakness. You do not get much market tension. Without other buyers in the process, price and terms often drift toward whatever the buyer finds easiest to accept. That can show up as a lower cash payment at closing, a long seller note, an earnout tied to future performance, or a handover period that keeps you attached longer than planned.

Personal history also complicates negotiation. Selling to someone you know can make it harder to press on working capital, vehicle treatment, accounts receivable, or what happens if service agreement customers leave after the handoff.

Direct sales save time when both sides are aligned. They get expensive when assumptions replace clear terms.

Path three with an M&A adviser

This route usually makes sense when the business is large enough to attract strategic acquirers, regional consolidators, or private equity-backed buyers.

Those buyers do not just buy a plumbing company. They buy route density, technician capacity, service agreement revenue, cross-sell potential, and a management team that can keep running after the founder steps back. An M&A adviser is useful when that bigger story is real and the numbers support it.

The process is more formal. There is usually tighter buyer targeting, more financial analysis, and more pressure on the business to prove its systems, reporting, and post-owner continuity. That extra work can pay off if the company has scale, management depth, and a credible case for growth under new ownership.

It is often too much process for a smaller founder-led shop.

Best fit: Businesses with stronger reporting, less owner dependency, and buyers beyond the usual local operator market.

A quick comparison

| Sale path | Usually suits | Main upside | Main trade-off |

|---|---|---|---|

| Broker | Small to mid-sized plumbing businesses | Broad buyer access and hands-on process support | Results depend heavily on the broker's trade experience |

| Direct sale | Known buyer situations | More control and less market exposure | Less pricing pressure and trickier term negotiation |

| M&A adviser | Larger or more layered deals | Targeted buyer outreach and stronger strategic positioning | More formal process and higher cost |

Choose the path that matches the business you have.

If your company still depends on you to sell work, calm big clients, and hold the team together, a polished process will not hide that. If you have recurring service revenue, a real office function, and field leadership that can operate without you, a wider and more competitive sale process can pay off.

Vetting Buyers and Navigating Negotiations

A buyer says your plumbing business is exactly what they want. They like the service agreement base, the vans, the phone volume, and the growth story. Then you ask how they plan to pay, who will run the field team, and what happens when you step out. That is usually where the serious buyers separate from the spectators.

Interest is cheap. Closing is what matters.

Start by controlling who gets what information, and when. A buyer does not need your full customer list, employee details, pricing by account, or every weakness in the operation on day one. They need enough to decide whether the opportunity fits. You need enough to decide whether they are credible.

Qualify before you disclose

The first job is simple. Find out whether the buyer can pay for the business and operate it after the deal closes.

That sounds obvious, but plenty of owners skip it because the conversation feels flattering. I have seen sellers hand over detailed P&Ls, customer concentration data, and staff information to people who were never in a position to buy.

Ask direct questions early:

- Funding: Is the purchase coming from cash, bank debt, investors, or seller financing?

- Deal size: Have they bought a business in this price range before?

- Trade fit: Do they understand service work, dispatch, call conversion, and technician management?

- Reason for buying: Are they an owner-operator, a competitor, or a financial buyer building a platform?

- Timing: Are they in an active process or just exploring options?

The answers shape how you handle the rest of the process. A strategic buyer may care most about route density, tech count, and customer overlap. An individual buyer will focus harder on training, seller support, and whether the office can function without you. A financial buyer will spend more time on reporting quality, recurring revenue, and who is staying after closing.

What buyers will test in diligence

Diligence is where the story meets the records.

Buyers will not just ask whether the business is profitable. They will test how the profit is produced, how repeatable it is, and how much of it depends on you. That matters more in plumbing than many owners expect because founder-led shops often carry hidden owner dependency. The owner sells the bigger jobs, calms down upset commercial accounts, approves pricing exceptions, and keeps the lead tech from leaving.

Those habits hurt transferability.

Common diligence pressure points

- Owner dependency: Who sells, who dispatches, who handles escalations, and who key customers trust.

- Service agreement quality: Buyers will want to see renewal rates, cancellation patterns, average revenue per member, and whether the agreements produce real call volume.

- Job profitability: They may review estimate accuracy, gross margin by job type, and callback rates.

- Customer concentration: A small group of commercial accounts can support value or create risk, depending on contract quality and relationship depth.

- Licensing, permits, and compliance: Missing paperwork or poor recordkeeping raises concern fast.

- Fleet and equipment condition: Deferred replacement turns into a price reduction or a closing adjustment.

- Team stability: Buyers want to know which technicians, field supervisors, and office staff are likely to stay.

Here's a useful video overview if you want to hear more about the sale process from a business transaction perspective.

Price is only one part of the negotiation

Owners tend to focus on the headline number. Experienced buyers focus on what they are paying, when they are paying it, what can reduce it later, and how much risk stays with the seller.

That is the right way to look at it.

A higher offer with a large earnout, loose working capital language, and aggressive reps and warranties can leave you worse off than a lower offer with cleaner terms. I tell plumbing owners to judge offers the way they would judge a job. The total price matters, but so do the exclusions, the payment schedule, the risk, and who is responsible when something goes wrong.

Key negotiation points usually include:

- Asset sale or share sale: This affects tax treatment, liability carryover, and what the buyer is taking on.

- Working capital: Define what stays in the business at closing, including cash, inventory, prepaid items, and payables if they are part of the deal structure.

- Seller transition support: Set the time commitment, duties, and boundaries in writing.

- Restrictive covenants: Non-compete and non-solicit terms should be reasonable in time, scope, and geography.

- Earnouts and holdbacks: If any money is deferred, the calculation method, reporting rights, and payment triggers need to be precise.

- Key employee retention: Buyers may ask you to help keep a service manager or lead estimator in place through closing.

The deal isn't done when the number sounds good. It's done when the terms are clear, finance is lined up, and both sides can perform.

Keep the negotiation factual. If a buyer finds a real issue, answer it with records and a practical solution. If they raise broad concerns without evidence and try to chip away at price, slow the conversation down and make them get specific.

Discipline helps sellers keep value. So does knowing which issues are normal and which ones signal trouble. A buyer who asks hard questions about service agreement churn or owner reliance may still be a good buyer. A buyer who stays vague about funding, avoids deadlines, and keeps reopening settled points usually creates problems later.

Closing the Deal and Planning Your Exit

Signing a letter of intent feels like the finish line. It isn't. It's the point where the legal, financial, and operational details get serious.

At this stage, owners should stop improvising.

Use the right support team

Your lawyer and accountant matter most near the end. They review the purchase agreement, flag risk, help you understand the structure, and make sure the deal documents match what was agreed.

That doesn't mean they should run the commercial negotiation for you. It means they protect you from loose drafting, bad assumptions, and expensive surprises.

What needs close attention

- Purchase agreement details: Make sure the assets, liabilities, exclusions, and obligations are spelled out properly.

- Payment terms: Check timing, conditions, and any holdbacks or deferred amounts.

- Restraints and warranties: Know exactly what promises you're making and for how long.

- Tax treatment: Get advice early enough to plan, not after the documents are already final.

Plan the handover like an operations project

The best transition plans are practical. They cover who gets told, when they get told, and what happens in the first weeks after completion.

A clean handover usually includes:

- Staff communication: Key team members should hear the news in a controlled, respectful way.

- Customer introductions: Important accounts need reassurance and continuity.

- Operational transfer: Logins, supplier contacts, phone systems, pricing tools, and workflow documents should be ready to hand over.

- Defined seller support: Put your transition role in writing so expectations are clear.

Prepare for your own exit too

Owners often focus so hard on selling that they forget to think about the morning after. For years, the business has shaped your schedule, decisions, and identity. Once it's sold, that changes fast.

Some owners stay involved for a period and enjoy helping the new owner settle in. Others want a clean break. Neither approach is wrong. What matters is deciding in advance so you don't drift into a role you never meant to keep.

If you've been wondering how to sell a plumbing business, the cleanest answer is this. Prepare early, value it accurately, present it properly, and don't confuse interest with a deal. Buyers pay best when they can see a business that works without the founder standing in the middle of every moving part.

If you're still building toward a future sale, GrowTradie can help keep your plumbing business visible and consistent while you focus on operations. For owners who want a stronger brand presence, steadier local awareness, and less day-to-day content hassle, it's a practical way to support the kind of business buyers like to see.