You've probably had this thought on the drive home after a long day. The phones still ring. The vans are busy. There's money coming in. But you're tired, and the idea of selling a plumbing business feels a lot harder than running one.

That's normal.

A lot of plumbing owners are excellent operators. They know how to price a job, calm down an unhappy customer, spot a weak apprentice, and keep work moving. Then they hit the point where they want out, or at least want options, and suddenly they're dealing with terms like SDE, EBITDA, earn-outs, due diligence, and transition planning. That can feel like stepping into someone else's trade.

I've seen the same pattern many times. A hands-on owner assumes the business will sell because the revenue looks strong. Then a buyer starts asking uncomfortable questions. Who holds the customer relationships. What happens when the owner leaves. Where are the documented processes. Can the office run dispatch, quoting, invoicing, and follow-up without the founder stepping in. That's where deals get stronger, weaker, or stall completely.

You don't need a finance degree to handle this properly. You need a clean plan, solid records, and an honest view of what a buyer is really buying.

Table of Contents

- Your Next Chapter Starts with a Plan

- Getting Your Business Sale Ready

- How to Value Your Plumbing Business

- Finding the Right Buyer or Broker

- Navigating the Offer and Negotiation

- Managing Due Diligence and Closing the Deal

- Starting Your Next Chapter with Confidence

Your Next Chapter Starts with a Plan

A plumber in his fifties usually doesn't wake up one morning and decide to sell by lunch. It builds slowly. The work is still there, but the pressure feels heavier. Staff issues wear you down faster than they used to. You start thinking more about freedom, family, health, or not being the one everyone calls when something goes wrong.

The first mistake many owners make is treating the sale like a job lead. They think someone will show up, look at the turnover, see the reputation, and make a sensible offer. That's not how business buyers think. A buyer is not just looking at what you built. They're looking at how safely they can take it over without watching profit leak out the moment you leave.

That changes the whole conversation.

If your business depends on you for quoting, key customer relationships, problem jobs, supplier decisions, team discipline, and cash flow visibility, then a buyer sees risk. If your team can run the day, your office knows the process, your numbers are clean, and your customers keep booking because the company works as a company, not as an extension of you, then a buyer sees an asset.

A plumbing business sells best when it looks less like a heroic owner story and more like a repeatable operating system.

Owners often focus on the wrong improvements. They repaint the office, tidy the yard, or replace uniforms, but leave core issues untouched. A serious buyer cares more about job costing, staff stability, documented workflows, recurring work, and whether the earnings can survive a handover.

The good news is that this is workable. You can prepare for a sale in the same way you'd prepare a major commercial project. Break it into stages. Get the facts straight. Fix what weakens the handover. Bring in the right help. Then go to market from a position of control, not guesswork.

Getting Your Business Sale Ready

Most owners start too late. They wait until they're exhausted, then decide to list the business and hope the market sorts it out. That approach usually leaves money behind because the problems that reduce value were built into the business long before the sale process started.

What buyers actually want

A buyer wants proof that the business can keep producing profit after you step back. That's why transition risk matters so much. If the business falls apart without the founder, the buyer either lowers the price, changes the terms, or walks.

One sector source notes that buyers pay more for businesses with recurring revenue, clean books, and systemized operations, while owner-heavy or project-heavy businesses trade at lower multiples. The same source also says buyers are increasingly screening for businesses that can operate without the founder, not just businesses with high top-line growth, because it lowers transition risk, as explained by Profitability Partners on selling a plumbing business.

Practical rule: You're not just selling a book of business. You're selling a machine that produces profit.

That machine needs to be visible. Buyers don't like mystery. If dispatch lives in one office manager's head, quoting rules change depending on your mood, and nobody follows the same service process, the business may still be profitable today, but it becomes harder to transfer tomorrow.

The sale-ready checklist that matters

The strongest prep work usually falls into a few plain categories.

Clean up the financial records: Your bookkeeping should tell a consistent story. If personal expenses run through the business, sort them out. If job margins are unclear, fix the reporting. If your accountant gives you year-end numbers but you can't explain month-to-month performance, that needs work.

Document how work gets done: Write down how leads are handled, how quotes are approved, how jobs are scheduled, how change orders are managed, how invoicing happens, and how follow-up is done. Use the tools your team already works in, whether that's ServiceTitan, simPRO, Fergus, Tradify, or a simpler stack. Fancy software doesn't solve bad process, but documented process inside familiar tools makes handover easier.

Reduce owner dependence: Start handing off decisions that don't need to sit with you. Let a service manager run the board. Let an estimator own quoting within clear guardrails. Let the office team handle customer communication without checking every message with the founder.

Tighten contracts and paperwork: Buyers will look at customer agreements, supplier terms, leases, equipment finance, employment agreements, and any subcontractor arrangements. Messy paperwork creates delays and distrust.

Build repeatable customer value: If all revenue comes from one-off jobs and reactive work, the business can still sell, but predictability helps. Service agreements, maintenance programs, and sticky customer relationships give a buyer more confidence.

Keep the team steady: A buyer notices whether key people are settled or halfway out the door. If your best dispatcher, estimator, or lead tech is frustrated and under-managed, fix that before a sale process starts.

A practical way to test readiness is simple. Take a week off and switch your phone off except for emergencies. If the business slows but keeps functioning, you're moving in the right direction. If everything jams up, that's the work to do.

Here's what doesn't work. Last-minute scrambling. Handwritten notes passed off as systems. “It's all in my head” explanations. Financial reports that need a verbal translation every time someone looks at them. Buyers don't pay top money for a rescue mission.

How to Value Your Plumbing Business

Valuation sounds more mysterious than it is. For most small trade businesses, it comes down to understanding the actual earning power of the company and then applying a market multiple to that earning base.

SDE in plain English

For many smaller owner-operated plumbing businesses, the key number is Seller's Discretionary Earnings, usually shortened to SDE. Think of SDE as the profit available to a working owner after adding back certain expenses that may not continue under a new owner.

In workshop-floor terms, it's not just “what the tax return says.” It's closer to “what this business produces for an owner once the numbers are cleaned up.” That can include things like the owner's salary and certain one-off or personal expenses that don't belong in the ongoing operation.

A useful way to think about it is property. Two buildings can look similar from the street, but buyers care about what they earn, how stable the tenants are, and how much work the new owner must do after settlement. Plumbing businesses are similar. Revenue gets attention, but earnings quality sets the tone.

According to Auxo Capital Advisors on selling a plumbing company, smaller plumbing businesses commonly trade in a 2x–4x SDE range. The same source notes that buyers usually ask for at least 3 years of federal tax returns, profit-and-loss statements, and balance sheets to verify that the earnings base is real and transferable. If a plumbing company produces $500,000 in SDE, that source says it might be valued at roughly $1.0 million to $2.0 million before deal-specific adjustments.

If you want a deeper breakdown of the mechanics, this guide on plumbing business valuation is a useful starting point.

What pushes value up or down

The multiple is where the argument happens. Owners naturally want the high end. Buyers naturally look for reasons to discount. The final number usually reflects risk, transferability, and quality.

A buyer leans upward when they see things like:

| Factor | Why it helps |

|---|---|

| Verifiable earnings | Clean records reduce debate and speed up trust |

| Stable service work | Ongoing customer demand feels safer than lumpy projects |

| Capable team | The business is less dependent on the seller |

| Documented systems | Handover looks manageable, not chaotic |

A buyer leans downward when they see the opposite. Owner dependence is the classic value killer. So are inconsistent books, weak middle management, and jobs that require the founder to step in whenever margins get tight or customers get difficult.

This video gives a useful overview of how buyers think about value and deal structure.

Don't anchor on turnover. Buyers buy earnings they can keep, not sales they have to rebuild.

A proper valuation is part maths, part judgment. The maths tells you the earning base. The judgment comes from asking whether that earning base survives the handover. That's why owners who systemize early usually negotiate from a stronger position.

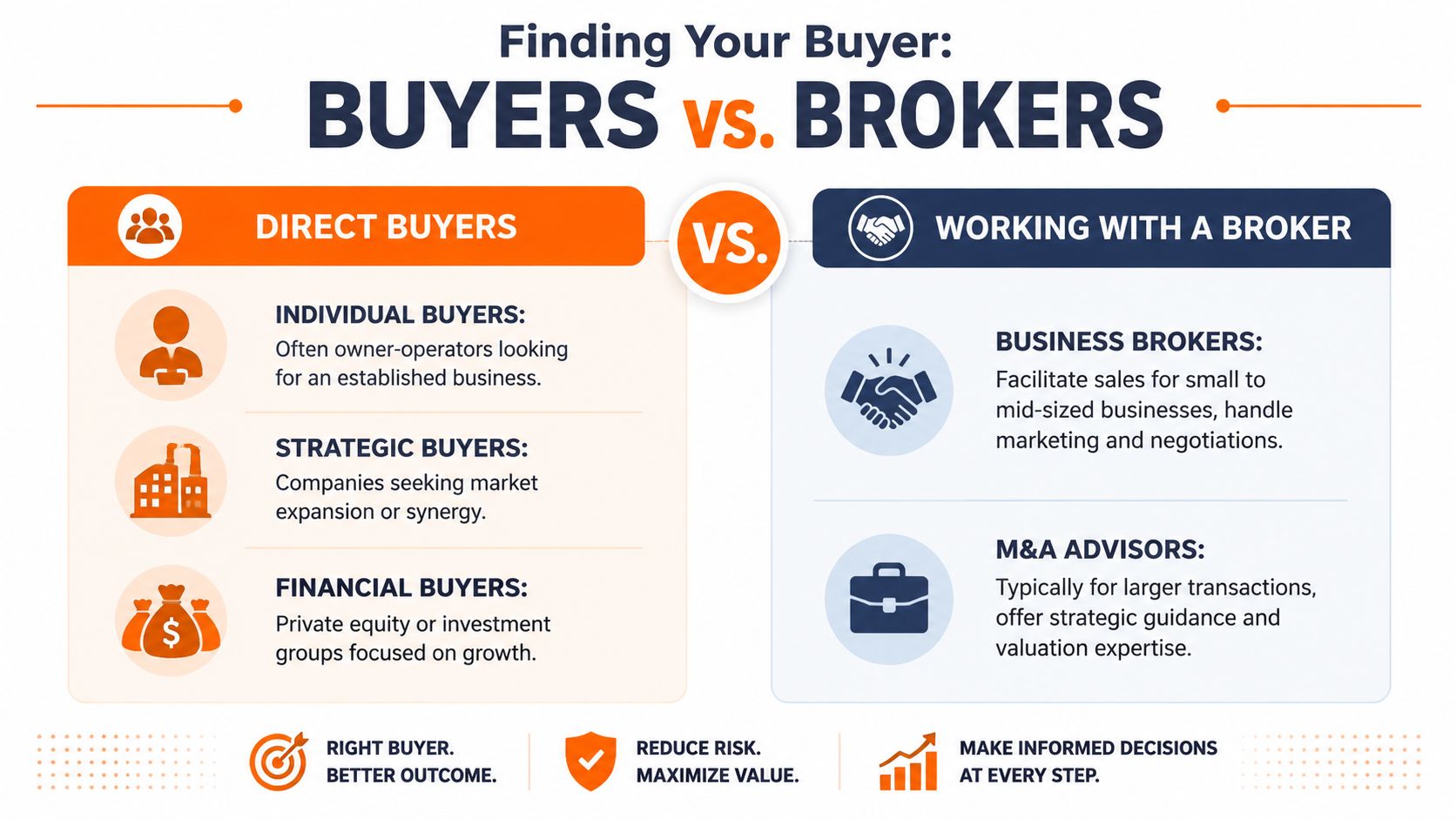

Finding the Right Buyer or Broker

Not every buyer is the right buyer. Some can pay well but move slowly. Some move quickly but want heavy seller involvement after closing. Some say all the right things early and become difficult once they get access to the books.

That's why I tell owners to think in fit, not just price.

The three buyer types

There are usually three broad buyer groups in this market, and each comes with a different mindset.

| Buyer type | Usually wants | Watch out for |

|---|---|---|

| Individual buyer | A business they can run day to day | They may rely on bank approval or need more support after closing |

| Strategic buyer | Territory, staff, customers, or service capacity | They may care more about overlap and integration than legacy |

| Financial buyer | A platform with growth potential and systems | They can be disciplined and demanding in diligence |

An individual buyer is often another ambitious operator. They like established revenue, a working team, and a recognizable local name. They may also need more hand-holding because they're buying themselves a job plus a business.

A strategic buyer is usually another company in the trade. They might want your technicians, your customer base, your service area, or your operational footprint. These buyers can be strong if your business fills a gap they already understand.

A financial buyer tends to focus on process, reporting, and leadership depth. They're usually less interested in a founder-centred operation. They want something that can scale under management.

When a broker earns their fee

A good broker is not just a listing agent. They act more like a process manager, filter, negotiator, and buffer. They package the business properly, keep discussions confidential, qualify buyers, control the flow of information, and stop time-wasters from draining your energy.

That matters because owners are often still running the business while trying to sell it. If you're the one chasing buyers, answering every question, drafting materials, and managing confidentiality, performance can slip at the exact moment buyers are scrutinizing it.

If you're weighing your options, this page on choosing a plumbing business broker can help frame the decision.

Ask direct questions before hiring anyone.

- How many trade businesses have you sold: You want someone who understands field staff, service agreements, vehicle fleets, and owner dependence.

- How do you qualify buyers: A real buyer and a curious competitor are not the same thing.

- Who handles the deal day to day: Sometimes the senior person wins your business and disappears.

- How will you protect confidentiality: Staff, customers, and suppliers shouldn't hear rumours before there's a signed deal.

- What happens if offers come in below expectation: You want strategy, not pressure.

A broker should make the sale calmer and cleaner. If they make it noisier, they're the wrong fit.

Some owners can sell directly, especially if a trusted buyer approaches and the deal is straightforward. But if there are multiple buyers, complicated terms, or sensitive staff concerns, professional handling usually pays for itself in reduced mistakes alone.

Navigating the Offer and Negotiation

The first offer often creates false confidence. Owners see a headline number and assume the hard part is done. In reality, the offer is just the framework. The details decide whether the deal works for you.

The headline price is not the whole deal

Most offers begin with a Letter of Intent, often called an LOI. It's a short document, but it carries a lot of weight. It usually sets out the proposed purchase price, what assets or shares are being bought, the expected handover period, confidentiality terms, and whether the buyer gets an exclusive window to complete due diligence.

Exclusivity matters more than many owners realise. Once you grant it, you're often off the market for a period while that buyer investigates the business. If they drag their feet or start retrading late, your negotiating power diminishes.

Emotion gets expensive. Owners read the offer as recognition for years of hard work. Buyers read it as an opening position in a commercial process. Keep your pride out of the markup notes. Let your lawyer, accountant, and broker be the ones who challenge terms.

Terms that deserve real attention

Price matters, but structure often matters just as much.

- Cash at closing: This is the cleanest money. The more that lands at settlement, the lower your future exposure.

- Seller financing: Sometimes this helps get a deal done, but it means you're still tied to the business risk after closing.

- Transition period: Be precise about what you'll do, how long you'll do it, and what happens if the buyer wants more access than agreed.

- Non-compete restrictions: These need sensible boundaries. You shouldn't sign away future options more broadly than necessary.

- Working capital expectations: Buyers often expect a certain level of normal operating cash, stock, or receivables to remain in the business at closing.

A lower offer with cleaner terms can beat a higher offer loaded with conditions, holdbacks, and vague post-sale obligations. I've seen owners chase the bigger number and then spend months tied to a buyer who keeps moving the goalposts.

Use a simple test. Ask, “What could go wrong for me after signing this?” If the answer includes delayed payments, open-ended consulting, unclear earn-out conditions, or aggressive restraint language, tighten it before you celebrate.

The best deal is the one you can live with after closing, not the one that looks best in the first email.

Good negotiation is steady, not theatrical. You don't need bluster. You need clarity, deadlines, and advisers who know where buyers usually push.

Managing Due Diligence and Closing the Deal

Due diligence sounds intimidating, but it's mostly verification. The buyer wants to confirm that the business they're buying matches the story they were told. If your preparation has been solid, this stage feels like admin. If not, it turns into stress.

What buyers usually ask for

Expect requests for core records and operational documents. That commonly includes financial statements, tax returns, customer lists, major contracts, leases, employee agreements, supplier arrangements, fleet or equipment details, and anything else that affects continuity.

Organise these before the buyer asks. Use a structured digital folder. Name files clearly. Keep versions current. Slow responses make buyers nervous, and nervous buyers start imagining problems.

If you want a sense of how buyers browse live opportunities and compare businesses, reviewing examples of a plumbing business for sale can help you see the market from their side.

How closing stays on track

Closing usually comes down to discipline. Keep communication tight. Answer questions directly. Don't improvise if you're unsure. Let your legal and accounting team handle technical issues rather than trying to smooth things over yourself.

The final purchase agreement is where the actual obligations sit. Read it carefully. Make sure it matches the commercial deal you thought you had. Then settlement becomes what it should be: funds move, documents are signed, ownership changes, and the handover begins.

A smooth close rarely happens by luck. It's the result of organised records, realistic negotiation, and a buyer who never had to wonder what they were walking into.

Starting Your Next Chapter with Confidence

Selling a plumbing business is not about getting lucky with one interested buyer. It's about building a business that someone else can take over with confidence. That starts long before the business goes to market.

The owners who do best usually do the same few things well. They clean up the books. They reduce dependence on themselves. They document how work gets done. They understand how value is judged. Then they negotiate carefully instead of getting distracted by the first big number.

If you're still in the early stage, that's fine. Start now. Tighten the operation. Make the business easier to run without you. Keep records that tell the truth clearly. Those steps help whether you sell next year, later on, or never.

You've already done the hard part. You built something worth buying. The rest is process, timing, and preparation. Handle those properly, and your exit can reward the years you put into it while giving you room for whatever comes next.

If you're focused on strengthening your plumbing business before a future sale, consistent visibility still matters while you're building systems, team depth, and a stronger brand. GrowTradie helps trade businesses stay active online with customized social content and auto-posting, so your business keeps showing up professionally while you stay focused on running the operation.